Email: sales@simple.works

The next 20% of affordable housing growth will not come from the cities you already know. It will emerge from micro-markets in Tier-2 and Tier-3 towns — and the HFCs that know which branches are outperforming, and exactly why, will own the decade.

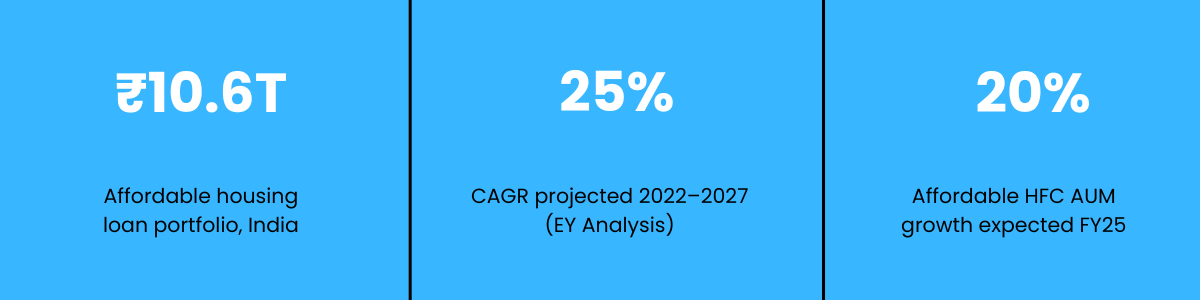

If you are a C-suite leader at an HFC, an NBFC, or a scheduled commercial bank with a housing finance vertical, the macro numbers are likely already on your dashboard. Affordable Housing Finance Companies have witnessed a robust recovery — with an anticipated AUM growth of 30% in FY25, and EY projects a 25% CAGR through 2027 for the segment. The Union Budget 2025–26 nearly tripled PMAY-Urban 2.0 allocations to ₹3,500 crore. The RBI brought the repo rate to 5.5% by mid-2025, and floating-rate home loans — 84% of the market — are already transmitting those cuts to borrowers.

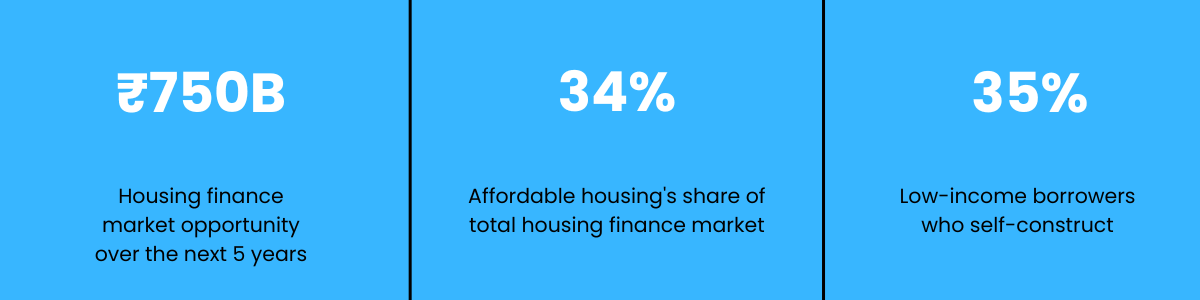

The demand signal is unmistakable. India’s urban population is expected to reach 40% by 2030, with most new homebuyers arriving not in Mumbai or Bengaluru, but in places like Nagpur, Indore, Lucknow, Surat, and the industrial corridor towns spinning up under Gati Shakti. The formal-wage economy is decentralizing; 60% of GDP creation is now estimated to be occurring outside the top metros.

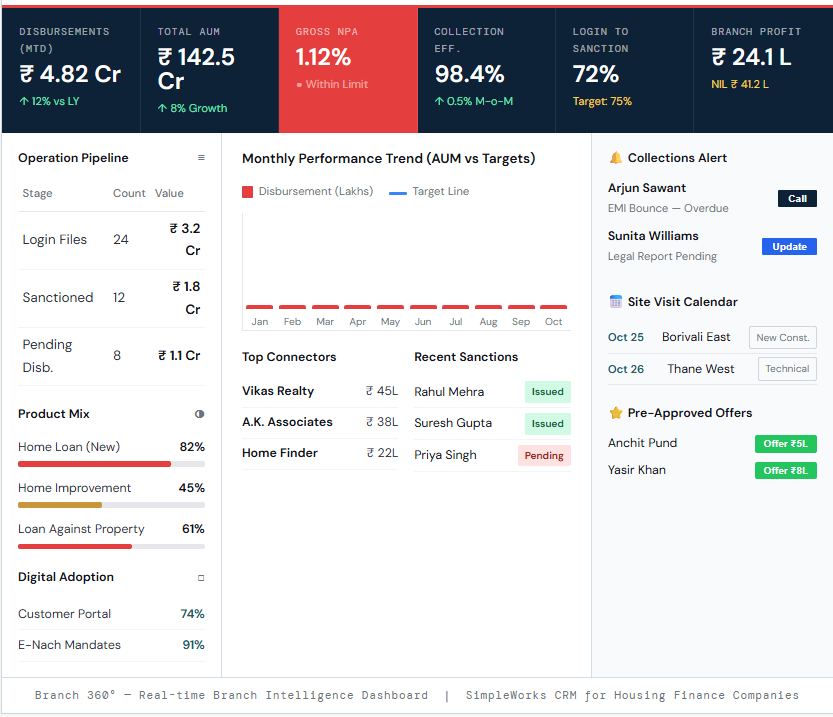

But here is what the macro numbers hide: within every growing market, there is enormous branch-level variation. One branch in your Tier-2 network may be running at ₹142 crore AUM with 98% collection efficiency and a Gross NPA of just 1.1%. Another, 40 kilometers away, may have rising SMAs, a Login-to-Sanction ratio of 60%, and a branch profit quietly eroding. Both look fine in your quarterly review slide.

The winners in this decade will not be those with the largest branch networks. They will be the institutions whose leadership can look at every branch — its disbursements, its pipeline health, its connector performance, its NPA trajectory — in real time, from a single screen, and make sharper resource allocation decisions accordingly.

The regulatory environment governing HFCs has fundamentally shifted. Since the Finance Act 2019 moved regulatory powers over HFCs to the Reserve Bank of India (RBI), with day-to-day supervision retained by the National Housing Bank (NHB), the compliance burden on leadership teams has intensified considerably.

⚠ REGULATORY ALERT — RBI HFC DIRECTIONS 2025

The RBI’s HFC Directions, issued in November 2025, consolidate and modernize prudential norms under the Scale-Based Regulation (SBR) framework. Key changes demanding board-level attention:

What this means at the C-suite level: NPA identification can no longer be a quarterly exercise. The days of relying on disconnected spreadsheets, siloed branch PDFs, and lagging MIS data are over — not just as a matter of operational efficiency, but as a matter of regulatory survival.

But here is the strategic insight most HFC leadership teams are missing: the same data discipline that protects you from regulatory censure is the same intelligence layer that reveals your next growth opportunity. A branch running at 98% Collection Efficiency, a 1.1% Gross NPA, and a Login-to-Sanction ratio trending toward the 75% target is not just a ‘healthy’ branch — it is a signal.

“A CRM that only tells you what went wrong is a compliance tool. A CRM that tells you which branch is about to outperform — and why — is a growth engine.”

Consider the challenge every HFC Regional Head faces today: sitting across multiple branches in their zone, they receive data in different formats, at different frequencies, with no easy way to compare performance, spot early stress, or identify which connector relationships are actually driving disbursements. The answer is not more reports. The answer is one intelligent, real-time dashboard — built specifically for regulated lenders.

The fundamental shift SimpleWorks enables for regulated lenders is this: your branch network is not just a distribution channel — it is your most valuable intelligence asset, if you give it the right platform.

Branch 360° is a real-time, branch-level intelligence dashboard designed specifically for Housing Finance Companies. Below is a live branch view — and more importantly, what it enables a leadership team to do:

Notice what a leadership team can now do from a single screen — without waiting for a Monday morning report or a quarterly portfolio review:

💡 THE C-SUITE INSIGHT: ONE DASHBOARD. EVERY BRANCH. THE SAME LENS.

The power of Branch 360° is not what it shows for one branch — it is what it enables when you apply the same lens across your entire network simultaneously. A CEO or Regional Head looking at 80 branches through Branch 360° can instantly rank branches by profit contribution, flag those with deteriorating Login-to-Sanction ratios, identify which connector relationships are underutilized, and surface the three branches that warrant immediate leadership attention — before the NHB review, not after it.

Let us be direct, because you are a decision-maker and your time is a scarce resource.

The CBRE Housing Affordability report of early 2026 confirms that household income growth is now outpacing property price appreciation for the first time since 2021 — meaning first-time buyers in Tier-2 and Tier-3 cities are entering the market with improving affordability. The demand window is open. The question is whether your branch network is positioned to capture it.

Right now, somewhere in your branch network, there is a Branch Manager sitting on a ₹1.1 Cr pending disbursement backlog with no visibility into which files are stalling and why. There is a connector generating ₹45L a month who is not receiving the engagement they deserve, and may be about to shift their business to a competitor. There is a borrower with a bounced EMI who will become an NPA in 30 days — but nobody has called them yet because the Monday morning report has not been compiled.

Branch 360° closes these gaps — not in quarterly reviews, but in real time.

Simultaneously, the RBI and NHB are not waiting. The HFC Directions 2025 are in force. The IRACP norms are live. The SBR framework is classifying your organization, and your obligations are escalating. The CRO you have appointed (or must now appoint) needs a platform that delivers real-time branch visibility, not a weekend of spreadsheet reconciliation before every board meeting.

The leaders who will define the next chapter of housing finance in India are those who understand that branch intelligence is not a cost center; it is the margin between growing profitably and growing blindly.

SimpleWorks is a CRM and AI solutions provider purposely built for regulated industries — including Housing Finance Companies, NBFCs, and Scheduled Commercial Banks. We do not build generic software and retrofit it to compliance. We start with the regulatory framework — RBI, NHB, IRACP, SBR — and build intelligence outward from there.

See how Branch 360° gives your leadership team real-time visibility across every branch in your network.

[1] EY India — https://www.ey.com/en_in/insights/financial-services/insight-into-the-present-and-future-of-indian-affordable-housing

[2] Metro India — https://www.metroindia.net/news/articlenews/future-of-affordable-housing-finance-36528

[3] Mordor Intelligence — https://www.mordorintelligence.com/industry-reports/india-home-mortgage-finance-market

[4] Mordor Intelligence — https://www.mordorintelligence.com/industry-reports/india-home-loan-market

[5] CBRE / New Kerala — https://www.newkerala.com/news/a/household-income-growth-expected-outpace-property-price-appreciation-642.htm

[6] RBI / NHB — https://www.nhb.org.in/wp-content/uploads/2026/01/Reserve-Bank-of-India-Housing-Finance-Companies-Directions-2025.pdf

[7] FinTax Blog — https://fintaxblog.com/rbi-housing-finance-companies-hfc-directions-2025/

[9] Lexology — https://www.lexology.com/library/detail.aspx?g=a07138f6-a49a-4cbc-954a-ea1be61832dd

[10] Ken Research — https://www.kenresearch.com/industry-reports/india-house-finance-market

[11] National Housing Bank (NHB) — https://www.nhb.org.in/supervision/directions/

[12] Vinod Kothari Consultants — https://vinodkothari.com/2024/01/housing-finance-companies-regulatory-framework-rbi-proposes-sectoral-harmonisation/