Email: sales@simple.works

Discover how CRM in banking transforms customer relationships, drives revenue growth, and ensures compliance. Learn implementation strategies for Indian financial institutions.

Let me tell you something I learned after two decades in the CRM trenches: Banking without a proper customer relationship management system today is like showing up to a Formula 1 race on a bicycle. Sure, you will eventually cross the finish line, but by then, everyone else has already popped the champagne.

The customers who once waited patiently in serpentine queues now expect instant gratification; whether they are applying for a home loan at midnight or checking their account balance while stuck in Bangalore traffic. And here’s the kicker: if you can’t deliver that experience, someone else will.

Banking CRM is specialized customer relationship management software that helps financial institutions manage customer interactions, centralize massive amounts of data, automate soul-crushing manual processes, and deliver personalized financial services; all while keeping the regulatory hawks happy.

Think of it as your institution’s nervous system. Every customer touchpoint, every transaction, every preference gets recorded, analyzed, and transformed into actionable intelligence. It’s not just about storing contact information anymore; it’s about understanding that Mrs. Sharma in Pune might be ready for a wealth management upgrade because her savings pattern changed six months ago.

The numbers don’t lie. The Indian banking CRM market is growing at a blistering 19.10% CAGR and is expected to hit $14.24 billion by 2034. That’s not just growth; that’s a revolution with a spreadsheet.

I will be honest: I have sat through enough vendor presentations promising “transformational customer experiences” to last three lifetimes. But here’s what genuinely happens when you implement banking CRM correctly:

The 360-Degree Customer View Your relationship manager can see everything about a customer in one place. Past transactions, ongoing disputes, investment preferences, that complaint they filed in 2019, even their preferred communication channel. No more “let me transfer you to another department” runaround.

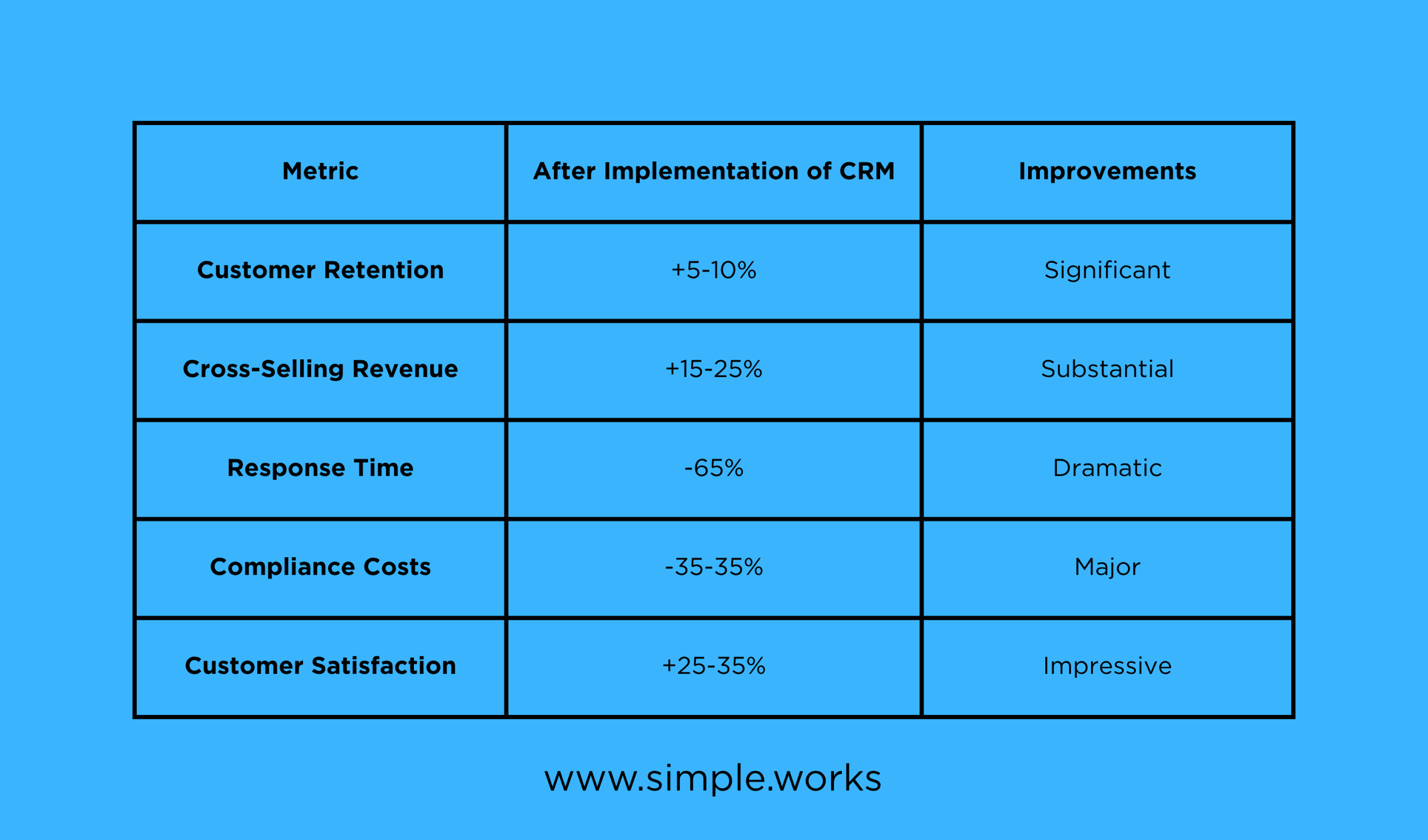

Response Time That Doesn’t Make People Want to Scream Modern banking CRMs can slash response times by 65%. When a customer reaches out, your team already knows who they are, what they need, and what they are likely to ask next.

Personalization That Actually Works With 90% of banks now adopting AI-driven personalization, you can offer that fixed deposit scheme to customers who actually need it, not blast it to everyone and hope for the best. The system learns patterns, predicts needs, and helps you be helpful rather than annoying.

Let me cut through the feature bloat. After implementing countless systems, here’s what genuinely moves the needle:

Customer Data Management: Handle millions of records without breaking a sweat. We are talking 13 million customers across 19 million accounts; the system needs to ingest data from your core banking system, payment platforms, even that legacy system from 1997 nobody wants to talk about.

Lead Tracking & Automation: Managing 700,000 leads while coordinating 16 million emails and 37 million SMS campaigns requires automated lead scoring, intelligent routing, and campaign management that doesn’t need a PhD to operate.

Compliance Reporting: Banking CRM compliance requirements are serious business. Your system should automate those 600+ RBI reports, track 1,000+ SLA analyses, and maintain audit trails that can survive regulatory scrutiny. Built-in compliance modules aren’t optional; they are mandatory.

Workflow Automation: If your team is manually processing loan applications, you are hemorrhaging productivity. Modern systems can handle 4,000+ automated processes, from digital onboarding with OCR verification to claims management.

Integration Capabilities: Your banking CRM integration with core systems needs seamless APIs connecting payment platforms, accounting software, telephony apps; the whole ecosystem. Cloud-based banking CRM solutions make this infinitely easier.

Absolutely. Small banks and regional financial institutions often think CRM is only for the big players with deep pockets. That’s outdated thinking. The best CRM software for small banks can deliver outsized returns precisely because smaller institutions are nimbler.

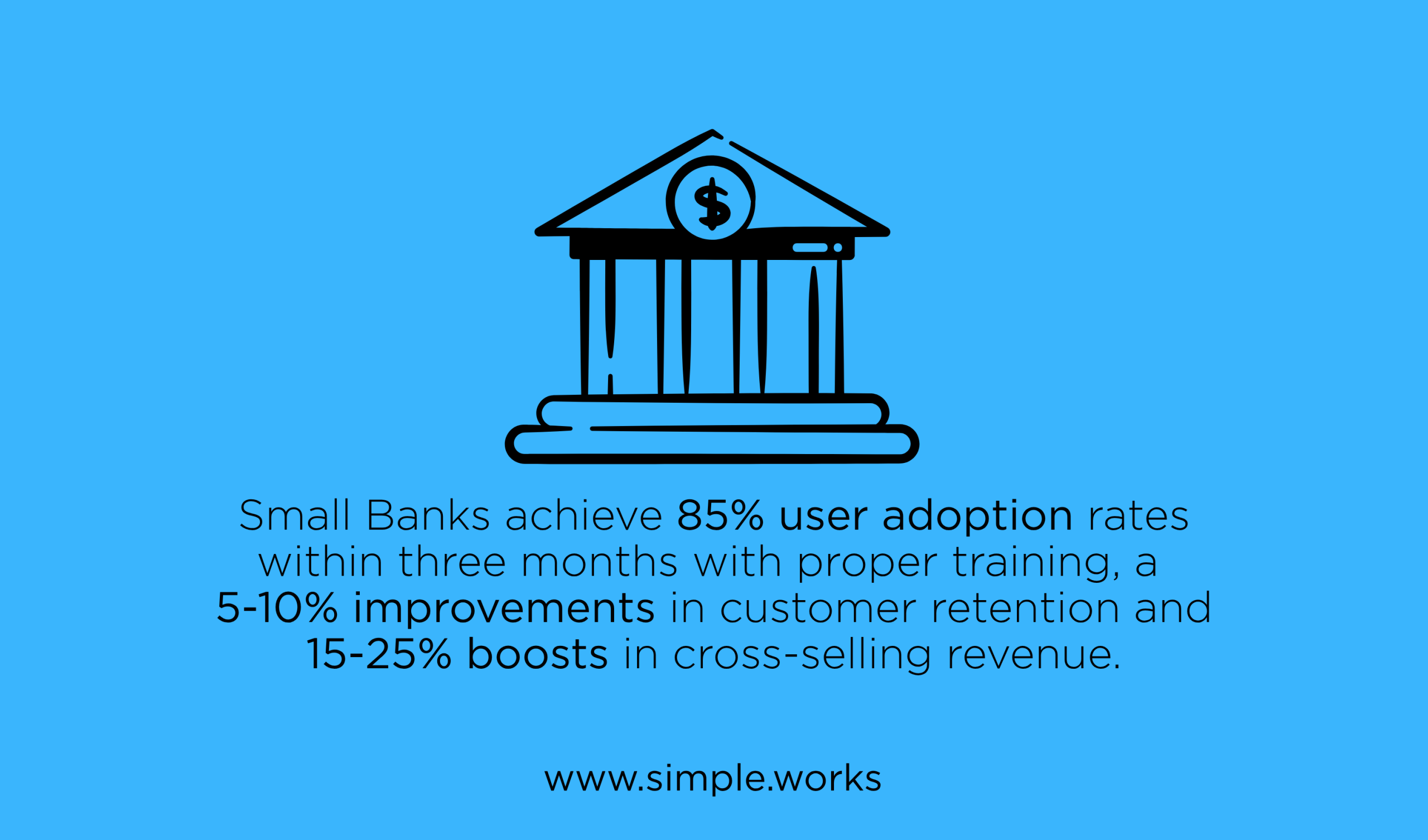

You can achieve 85% user adoption rates within three months with proper training. You will see 5-10% improvements in customer retention and 15-25% boosts in cross-selling revenue. Here’s the math that matters: for every rupee you invest in CRM, you are looking at ₹8.71 in returns, with payback periods between 6-18 months.

Let’s address the elephant in the boardroom. Banking CRM implementation isn’t always smooth sailing:

Data Migration Nightmares: Moving decades of customer data from disparate legacy systems is like performing open-heart surgery while the patient runs a marathon. You are looking at 12-15 system integrations on average, with implementation timelines stretching to six months.

User Adoption Resistance: Your relationship managers who have been doing things “their way” for twenty years won’t suddenly become CRM enthusiasts. Change management isn’t just training; it’s psychology and incentives.

The Cost Question: CRM costs vary wildly; from ₹2,500-7,000 per user per quarter for basic solutions to enterprise implementations requiring custom pricing. Then there’s the 15-20% of your budget for security and compliance.

Not necessarily. For smaller institutions, CRM management can be allocated to existing employees with proper training. But here’s my advice: if you are a larger institution with complex operations, invest in dedicated CRM administrators. The ROI of having someone who truly owns the system is immense.

The ownership question is interesting too. I have seen CRM succeed when marketing and retail departments handle administration, but with input from all business lines through a CRM committee. It can’t be an IT project alone; it needs to be a business transformation initiative.

Let me show you what’s actually achievable:

Operational Efficiency: 20-30% cost reduction through process automation, with 200,000+ monthly tickets resolved efficiently through automated workflows.

Revenue Impact: 40-60% improvement in cross-selling success rates with 95% precision in customer segmentation for targeted campaigns.

Compliance & Risk: 45% improvement in fraud detection accuracy and 60% faster audit processes with automated reporting.

After implementing systems across 15 countries, here’s my framework:

Look, I am not going to sugarcoat this: implementing CRM in banking is challenging. It requires investment, commitment, and organizational change that makes people uncomfortable. But here’s the reality; your competitors are already doing it, your customers already expect it, and the regulatory environment increasingly demands it.

The Indian banking sector is at an inflection point. Digital transformation isn’t a buzzword anymore; it’s the price of admission. Whether you are a public sector bank serving millions or a nimble regional player carving out your niche, customer relationship management banking is no longer optional.

The institutions that will thrive in the next decade aren’t the ones with the most branches or the longest history. They are the ones that know their customers intimately, serve them proactively, and make banking feel effortless.

Ready to transform your banking CRM strategy? The market is moving at 19.10% CAGR. The question isn’t whether to implement CRM; it’s whether you can afford to wait another quarter while your competition pulls ahead.

About the Author: With over 20 years of experience implementing CRM solutions across banking and financial services, I have witnessed firsthand how the right technology transforms institutions from transactional entities into customer-centric powerhouses.